File:Securitization Market Activity.png

{kind=link}

{kind=link}

{kind=link}

原始檔案 (960 × 720 像素,檔案大小:79 KB,MIME 類型:image/png)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

摘要

|

File:Securitization Market Activity.svg是本檔案的向量版本。 如果品質不低,就應該優先使用該檔案,而非PNG檔案。

File:Securitization Market Activity.png → File:Securitization Market Activity.svg

更多資訊請參閱Help:SVG/zh。 |

|

| 描述 |

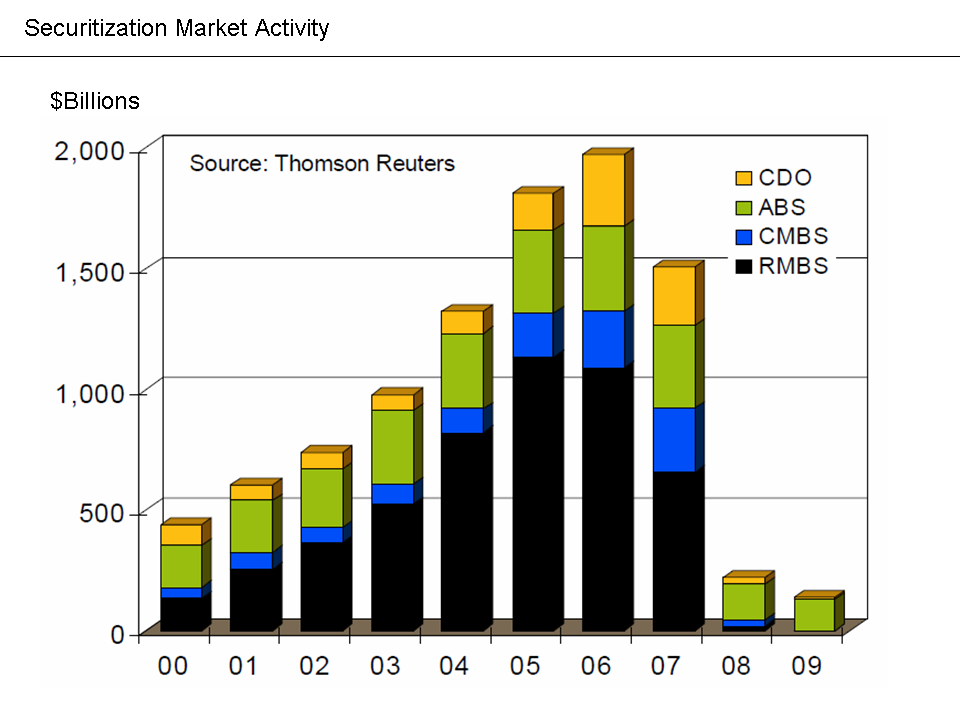

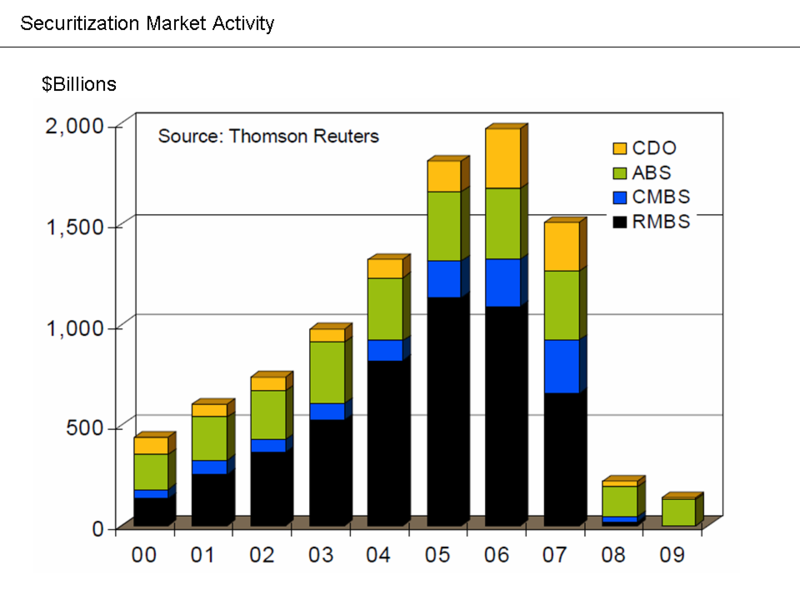

English: Image from Economist Mark Zandi's FCIC Testimony

ExplanationFrom Economist Mark Zandi's January 2010 testimony to the Financial Crisis Inquiry Commission: "The securitization markets also remain impaired, as investors anticipate more loan losses. Investors are also uncertain about coming legal and accounting rule changes and regulatory reforms. Private bond issuance of residential and commercial mortgage-backed securities, asset-backed securities, and CDOs peaked in 2006 at close to $2 trillion...In 2009, private issuance was less than $150 billion, and almost all of it was asset-backed issuance supported by the Federal Reserve's TALF program to aid credit card, auto and small-business lenders. Issuance of residential and commercial mortgage-backed securities and CDOs remains dormant."[1] Banks and other financial institutions packaged various types of loans (including mortgages) into securities and sold them to global investors. This is called securitization. In exchange for purchasing the investment, the investor receives a right to the cash flows from the underlying loans specified for the security. The chart shows how this financing source dried-up, meaning that non-prime mortgages and other types of loans could not be originated and sold to investors. |

| 來源 | http://www.fcic.gov/hearings/pdfs/2010-0113-Zandi.pdf |

| 作者 | Farcaster (talk) 04:36, 10 October 2010 (UTC) |

授權條款

此作品在美國屬於公有領域,因為其是由美國政府的官員或僱員,基於其個人公務目的製作的作品,參考美國法典第17篇第1章第105條。

注意︰本模板僅適用於美國聯邦政府的原創作品,不適用於任何美國州、屬地、聯邦個體、縣、市或任何次級政府的作品。本模板也不適用於1978年以後由美國郵政署出版的郵票圖案(參看美國版權局實踐綱領第313.6(C)(1)條)。也不適用於部分美國硬幣;參看美國鑄幣局使用條款。 |

| |

| 此作品無已知的著作權限制,亦不受所有相關和鄰接的權利限制。 | ||

原始上傳日誌

{kind=link}

- 2010-10-10 04:36 Farcaster 960×720× (81241 bytes) {{Information |Description = Image from Economist Mark Zandi's FCIC Testimony |Source = http://www.fcic.gov/hearings/pdfs/2010-0113-Zandi.pdf |Date = ~~~~~ |Author = ~~~~ |Permission = |other_versions = }}

檔案歷史

點選日期/時間以檢視該時間的檔案版本。

| 日期/時間 | 縮圖 | 尺寸 | 使用者 | 備註 | |

|---|---|---|---|---|---|

| 目前 | 2010年10月14日 (四) 01:07 | | 960 × 720(79 KB) | Hideokun | {{Information |Description={{en|Image from Economist Mark Zandi's FCIC Testimony<br/> == Explanation == From Economist Mark Zandi's January 2010 testimony to the en:Financial Crisis Inquiry Commission: "The securitization markets also remain impai |

檔案用途

下列頁面有用到此檔案:

全域檔案使用狀況

以下其他 wiki 使用了這個檔案:

- cs.wikipedia.org 的使用狀況

- en.wikipedia.org 的使用狀況

- fa.wikipedia.org 的使用狀況

- hy.wikipedia.org 的使用狀況

- it.wikipedia.org 的使用狀況

- ja.wikipedia.org 的使用狀況

- vi.wikipedia.org 的使用狀況

{kind=link}