File:Securitization Market Activity.png

{kind=link}

{kind=link}

{kind=link}

原始文件 (960 × 720像素,文件大小:79 KB,MIME类型:image/png)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

摘要

|

File:Securitization Market Activity.svg是此文件的矢量版本。 如果此文件质量不低于原点阵图,就应该将这个PNG格式文件替换为此文件。

File:Securitization Market Activity.png → File:Securitization Market Activity.svg

更多信息请参阅Help:SVG/zh。 |

|

| 描述 |

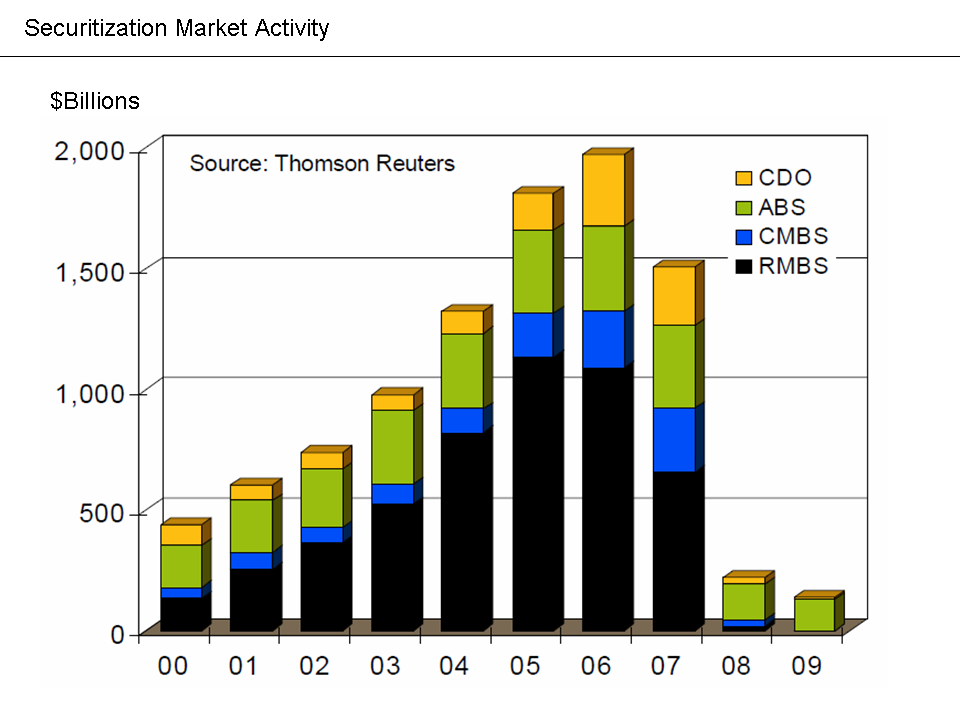

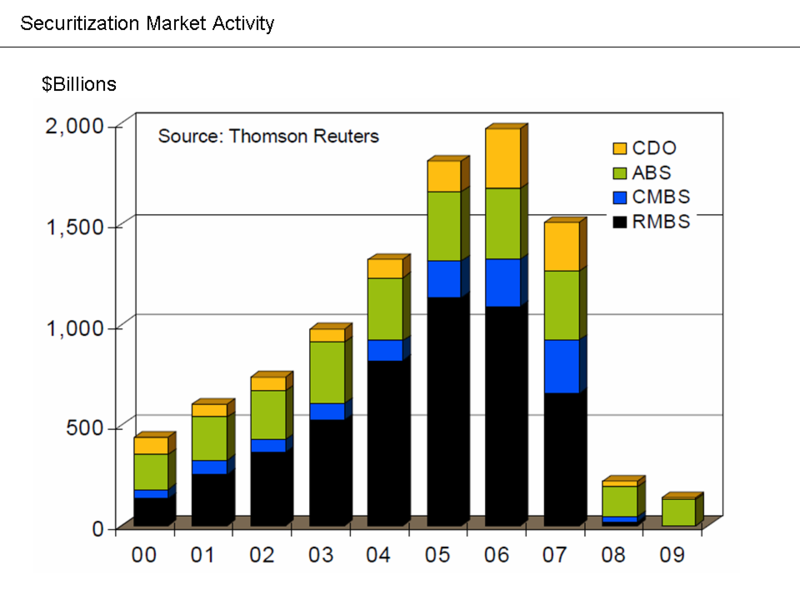

English: Image from Economist Mark Zandi's FCIC Testimony

ExplanationFrom Economist Mark Zandi's January 2010 testimony to the Financial Crisis Inquiry Commission: "The securitization markets also remain impaired, as investors anticipate more loan losses. Investors are also uncertain about coming legal and accounting rule changes and regulatory reforms. Private bond issuance of residential and commercial mortgage-backed securities, asset-backed securities, and CDOs peaked in 2006 at close to $2 trillion...In 2009, private issuance was less than $150 billion, and almost all of it was asset-backed issuance supported by the Federal Reserve's TALF program to aid credit card, auto and small-business lenders. Issuance of residential and commercial mortgage-backed securities and CDOs remains dormant."[1] Banks and other financial institutions packaged various types of loans (including mortgages) into securities and sold them to global investors. This is called securitization. In exchange for purchasing the investment, the investor receives a right to the cash flows from the underlying loans specified for the security. The chart shows how this financing source dried-up, meaning that non-prime mortgages and other types of loans could not be originated and sold to investors. |

| 来源 | http://www.fcic.gov/hearings/pdfs/2010-0113-Zandi.pdf |

| 作者 | Farcaster (talk) 04:36, 10 October 2010 (UTC) |

许可协议

此作品在美国属于公有领域,因为其是由美国政府的官员或雇员,基于其个人公务目的制作的作品,参考美国法典第17篇第1章第105条。

注意︰本模板仅适用于美国联邦政府的原创作品,不适用于任何美国州、属地、联邦个体、县、市或任何次级政府的作品。本模板也不适用于1978年以后由美国邮政署出版的邮票图案(参看美国版权局实践纲领第313.6(C)(1)条)。也不适用于部分美国硬币;参看美国铸币局使用条款。 |

| |

| 本文件已被确认为免除已知的著作权法限制(包括所有相关权利)。 | ||

原始上传日志

{kind=link}

- 2010-10-10 04:36 Farcaster 960×720× (81241 bytes) {{Information |Description = Image from Economist Mark Zandi's FCIC Testimony |Source = http://www.fcic.gov/hearings/pdfs/2010-0113-Zandi.pdf |Date = ~~~~~ |Author = ~~~~ |Permission = |other_versions = }}

文件历史

点击某个日期/时间查看对应时刻的文件。

| 日期/时间 | 缩略图 | 大小 | 用户 | 备注 | |

|---|---|---|---|---|---|

| 当前 | 2010年10月14日 (四) 01:07 | | 960 × 720(79 KB) | Hideokun | {{Information |Description={{en|Image from Economist Mark Zandi's FCIC Testimony<br/> == Explanation == From Economist Mark Zandi's January 2010 testimony to the en:Financial Crisis Inquiry Commission: "The securitization markets also remain impai |

文件用途

以下页面使用本文件:

全域文件用途

以下其他wiki使用此文件:

- cs.wikipedia.org上的用途

- en.wikipedia.org上的用途

- fa.wikipedia.org上的用途

- hy.wikipedia.org上的用途

- it.wikipedia.org上的用途

- ja.wikipedia.org上的用途

- vi.wikipedia.org上的用途

{kind=link}